In 2008, Satoshi Nakamoto established the first digital bitcoin transaction by mining the so-called genesis block. This was to be the beginning of a new era for money and the payment system, but the story did not develop according to the original aims of the pseudonymous bitcoin creator. Digital currencies really have the potential to change the economic landscape. The problem is that, under capitalist conditions, they will not be used to help ordinary people, but rather, the profiteering bankers. Note: this article was written in December 2020.

Cryptocurrencies: an infantile disorder

Digital currencies have been around for a while, although only the birth of blockchain technologies facilitated their success. As Marxists predicted, their potential to change the payment system has not materialised because these technologies were not introduced as a part of a general plan to develop the economy in the interests of the whole population, but rather to facilitate profits for the few. As a result, they have become just another financial bubble.

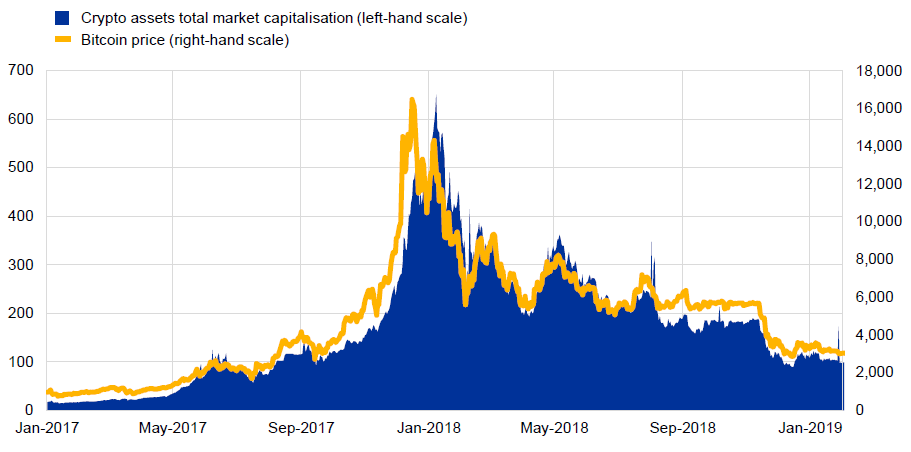

After the peak in January 2018, the market capitalisation of these assets collapsed. After a while, they experienced a recovery, as in any classical financial bubble. Recently, their value grew rapidly, as has that of other financial assets, thanks to the help of the central banks. For instance, the Dow Jones Index in the last six months grew around 20 percent.

Bitcoin and other cryptocurrencies are too unstable to be viable as money in the normal economy / Image: ECB

Bitcoin and other cryptocurrencies are too unstable to be viable as money in the normal economy / Image: ECB

Ups and downs of cryptocurrencies do not change their economic role, on the contrary, they cement it. The reason why bitcoin and the like never had a chance to replace ordinary currencies is not technological, but economic and social. Money is not, as in the fantasy world of mainstream economics, a technical device discovered to ease the awkwardness of barter, but a social relationship between classes, and in particular between the labour force (workers) and the owners of the means of production (capitalists). This relationship is the core fabric of the productive system, therefore its defence is the most sacred duty of bourgeois institutions, from the central bank to the army.

The bitcoin project, created by followers of anarcho-capitalist ideas, was meant to step in after 2008. Its creators believed the global financial crisis and subsequent state intervention would destroy the value of official currencies. They thought, in line with childish monetarist wisdom, that as central banks created a lot of money, automatically inflation would skyrocket in a matter of months. This would lead people to abandon dollars, euros and gold and bitcoins.

It seemed as if Hayek’s old dream of denationalising (i.e. privatising) money was becoming a reality. This did not happen, and bitcoins remained on the fringes of the ordinary economy. The fact that the number of digital currencies multiplied, from tens to thousands, paradoxically confirmed that none of them was able to become a true currency.

The immediate factor behind the failure of cryptocurrencies was their instability. For instance, bitcoin increased its price 20 times in 2017. Money should be stable, to permit its use as a unit of exchange and accounting, otherwise it is useless as money (even if it can be used as a financial asset, among others). It does not help that mining bitcoin takes days and days of continuously running hundreds of thousands of very powerful computers, thus expending an enormous amount of energy, already surpassing the whole output of Switzerland in 2019. Financial speculation that consumes the energy of a country of almost 9 million people is the very definition of capitalist waste.

The fate of cryptocurrencies has also shown a deeper point: capitalism is an unstable system. Even without major crises, such as the 2008 global financial crisis or the pandemic, it needs endless state interventions to tackle its unstable features and to help the capitalists to control the situation. In the sci-fi world of cryptocurrency, it was sufficient to eliminate human intervention and let software do all the work to have the problem solved. The reality has painfully dispelled this infantile illusion.

An uncertain compromise: the stablecoins and Libra

Cryptocurrencies like bitcoin never had the chance to become widely accepted by firms and households as a means of payment for the simple fact that they are too unstable to allow for the exchange of commodities. Moreover, governments and central banks were not willing to renounce their control of the currency, which is a vital aspect of economic regulation. Strong currencies come from a strong economy, but also vice versa.

However, digital currency still seemed a great idea to many. A new generation of digital currencies came about: the so-called stablecoins. Their technology is similar to that of the ordinary cryptocurrencies but they contain a stabilising mechanism. Their value is connected to a traditional currency or a tranche of traditional currencies (a method called collateralisation) that makes a stablecoin similar to a typical monetary mutual fund, made up of short-term assets in dollars, euros and so on. Stablecoins promise (although this is not legally binding) convertibility with the dollar or other currencies, and this allows them to be by far more stable than bitcoin. But for all their stability, this new generation of cryptocurrencies was not gaining much success as an alternative currency either, until Facebook stepped in.

When, in June 2019, Facebook and other big firms presented the Libra Association, it was immediately clear that the world of digital currencies was changing forever. The Association published a whitepaper: “An Introduction to Libra”, that was comic for how much corporate hypocrisy it contained. The promoters explained to the world that they were introducing the first, stable world currency for humanitarian reasons. In fact, they noted: “large swaths of the world’s population are still left behind — 1.7 billion adults globally remain outside of the financial system with no access to a traditional bank”. To help the poor to access cheap and reliable financial services, Facebook and the others were offering Libra to the planet. To have a global stablecoin, the new currency was based on a tranche of currencies. At first, the (vague) idea was to have a value based half on dollars, and half on the yen, euro, pound and other minor currencies.

Mark Zuckerberg, the CEO of Facebook, was attacked by members of Congress over his proposals for Libra, who took the chance to remind him of all the past misconduct of his firm regarding data security / Image: Anthony Quintano

Mark Zuckerberg, the CEO of Facebook, was attacked by members of Congress over his proposals for Libra, who took the chance to remind him of all the past misconduct of his firm regarding data security / Image: Anthony Quintano

Although Libra was backed, at first, by strong names, such as Visa, Mastercard and Vodafone, it rapidly became clear that the project was going nowhere. The immediate reason was that governments and central banks were not keen to give to a private project such power over the world monetary system. Moreover, given that Facebook had a long history of total indifference on privacy issues, to say the least, it was also obvious that the financial data of everyone using Libra would have been on sale to the highest bidder.

Traditional banks were also not very happy to see new competitors eating away at their revenues from payment systems that generate around $2,000 billion a year. Besides all these aspects, it was an opportunity to take revenge for all the scandals Facebook had been involved in so far. During his hearing in the fall of 2019 at the US Senate, Mark Zuckerberg, the CEO of Facebook, was attacked by a host of very critical members of Congress, who took the chance to harshly remind him of all the past misconduct of his firm. There were also critical observations by financial regulators on the lack of security in the project, in terms of money-laundering and privacy regulation.

The barrage of critics forced Libra on the retreat. After a while, the Association announced a drastic downgrading of the scope of the project, while many high-profile members were abandoning it. In April 2020, a new version of the whitepaper came out. The main difference with the original project is that Libra is now proposed as a national stablecoin. In other words, Libra was no longer envisioned as a single global currency but as a digital version of the dollar, the euro, etc, backed by a fund with assets denominated in that currency. The Association also made many humble remarks on how it was willing to collaborate with financial regulators. It is now very unlikely that Libra will see the light of day any time soon.

Coming of age: the central bank digital currencies

While Libra was relaunched as basically another PayPal, governments and central banks were starting to discuss the future of public digital currencies.

Although central banks have discussed projects for digital currencies before, like the “Dinero electrónico” of the Central Bank of Ecuador in 2014, these projects were unsuccessful. Libra changed the landscape. While the Association was reorganising their ideas, international financial regulators issued a number of documents on stablecoins and digital currencies. For instance, in April 2020, the Financial Stability Board called on governments, central banks and financial regulators to face the challenge of digital currencies and in particular of global stablecoins. Even if none of them is singled out in the document, it is clear that the FSB document was an answer to the threat posed by Libra to global financial stability.

Although it is true that Libra could be easily used for fraud and money laundering, this is not the reason why it has been stopped. Most of the existent cryptocurrency exchanges have weak anti-money laundering controls, as well as scant identification procedures. The problem was the scale of the project, which risked destabilising the global financial system (which is already very fragile); and the threat to the profits of the existing banks.

Out of this debate emerged a third kind of cryptocurrency: central bank digital currencies. The projects are of different types, but we can focus on the simplest one: a central bank universal current account. The central bank could create a current account for every individual and firm in the country, so that every financial relationship in the system could be easily regulated via the books of the central bank. The advantages of such a public digital currency are obvious. First of all, its efficiency: every payment could take place instantly and cheaply. No more cash, checks, debit cards and so on. Secondly, every state payment to citizens could rapidly reach its target. For instance, during the pandemic, in Italy and elsewhere, there have been many polemics over the fact that the unemployment benefits and other state aids were very late, forcing many families to remain in debt, while continuing with ordinary payments. Under a universal account system, governments could pay instantly and can also easily take money from people’s accounts, like taxes for instance.

This universal state bank could make loans and receive deposits, just like any commercial bank. The (positive and negative) interest rates on the accounts could substitute the present form of monetary policy. For instance, the central bank could lower interest rates on deposits to push consumption or lower interest rates on loans to push investment.

Finally, given that cash would almost disappear, the grey and black economy, which account for between 10 percent and 30 percent of the OECD economies, would be heavily hit. More generally, the state would have a precise idea of the cash flows of every firm of the country. Of course, the incredible capacity of capitalists to bypass their own laws would not disappear, but they would have many more problems when it comes to escaping public controls for fiscal or criminal laws purposes.

A central bank digital currency would be a secure and effective new payment system technology. It seems like an Egg of Columbus in the making. In fact, every important central bank is engaging in some project around digital currency. However, this is basically a defensive move against Libra and they are not willing to really create a universal account system.

It is not difficult to understand why. A central bank digital currency could sweep out the entire banking system, which would become useless overnight. The profitable services offered by commercial banks would be offered instead by the central bank. Why on earth would a client stay with a commercial bank that offers the same services at greater cost? The universal account system could be used to promote the inclusion of the poorest and vulnerable people, who are now excluded from the banking system, by lowering its cost. It would also be very interesting for retailers and small traders, who would no longer be squeezed by the banks.

In other words, the clients of the commercial banks would drop to almost nil very quickly. Even if the universal account system only offered basic financial services, not many people actually need sophisticated financial services. This would mean that the banks would lose the bulk of their deposits, i.e. their core source of liquidity. Their business model would collapse. Every secret that banks keep for their wealthy clients would be at the disposal of public authorities. Big banks, criminal organisations and wealthy people would receive a devastating blow from such a change, and as they constitute an important part of the ruling class, the change will not come as long as they are in power.

Bourgeois strategists know that a retail central bank digital currency would be a game changer, so they are afraid of the idea. For instance, a recent document from the Bank of England points out:

“An approach to CBDC [central bank digital currency], where the Bank of England does everything, with no private sector involvement, is unlikely to meet most of our design principles. Such a CBDC may be resilient, fast and reliable. But it would not be open to competition, may not support innovation, and would not be designed around the respective strengths of the Bank and private sector…

“This shrinking of the banking sector’s balance sheet is known as ‘disintermediation’… If disintermediation were to occur on a large scale, that would either imply a large fall in lending or would require banks to seek to borrow significantly more from the Bank of England. This could have profound implications for the structure of the banking system and the Bank’s balance sheet.”

In other words, a public digital currency would reveal the uselessness of the private banking system, forcing the private banks to beg the central bank for liquidity. Needless to say, destroying financial capital does not meet the central bank’s “design principles”. So even if they are forced to introduce some form of public digital currency, they will limit it as much as they can, probably only to flows among banks.

The case of China

The shyness of imperialist countries toward adopting a central bank digital currency is not completely shared by the People’s Republic of China, where there are already giant payments services such as WeChat and Alipay. This issue has become an important battleground between the state and private big firms. In fact, the outlawing of most digital currency activity occurred in tandem with research for a state-backed digital currency, although rules against digital currencies already started in 2013.

China already has giant digital payments services / Image: Pixabay

China already has giant digital payments services / Image: Pixabay

In October 2020, the central bank proposed a new version of the “People’s Bank of China Law”, preparing the landscape for a public digital currency. The aims of this project are twofold. Domestically, the goal is to defend state money against private cryptocurrencies, and more generally to exert more control over the private bourgeoisie. A bigger economic role for the state after the pandemic will be widespread, but in China this entails a ferocious fight between state-owned enterprises and private bourgeois corporations.

This fight also explains the sensational failure of the market flotation of Ant Group, which was going to be the biggest share offering in history, and was dramatically suspended just two days before dealings were to start in Shanghai and Hong Kong. We can ignore the formal reasons: Chinese regulators stepped in to prevent the dominant payment company in China from becoming even more powerful. On the other side, a public digital currency will allow the Chinese central bank to monitor money flows in such a huge economy, providing the government with an unprecedented set of economic data.

On an international level, the public digital currency is meant to strengthen the role of yuan, it might be “the long-expected but elusive shock that finally dislodges the US dollar from its decades-long dominance in global trade and finance”, as the IMF chief economist Gopinath observed. Becoming the first state-backed digital currency, the yuan could be ready for when other countries decide to join. China will be able to create its own international payment architecture, based on the digital yuan, at the expense of Western architectures that are slowed down by the opposition of large banks.

So, while Western central banks and governments are waiting, to avoid a frontal clash with financial capital, China can rapidly proceed to such an innovation. In fact, the People’s Bank of China already introduced a pilot form of its digital currency in Shenzhen, with plans to use it in the area of Beijing during the 2022 Winter Olympics. In October 2020, already more than three million transactions worth 1.1 billion yuan have been processed using the digital currency.

A Bolshevik road to cryptocurrencies

Among the many flaws of modern bourgeois economics, including its “alternative” strands, is the fact that the class nature of the state and of its institutions, like central bank and money, are completely ignored. They are given no class content also because classes, under these theories, do not even exist. This allows right-wing economists to support the status quo and left-wing economists to not propose anything really dangerous for the ruling class.

Their stance on money derives from this attitude. On the one hand, we have the childish dream of an automatic stabiliser of capitalism. These fantasies, either in the realm of “market discipline” in financial regulation or in the digital world through cryptocurrencies, are now exposed as useless. On the other hand, we have the frequent lamentations of Keynesian economists: why don’t governments just invest more to reduce unemployment? Why don’t they regulate the financial sector more strictly? In a phrase: why don’t governments help the population? The answer is obvious: unless they are forced to act otherwise by a mass movement from below, governments only regulate the economy to maximise corporate profits.

This is what monetary and fiscal policy are all about. Whether it’s quantitative easing or public investment, whatever form the state intervention takes, the final goal is the accumulation of wealth in the hands of big business, as we saw with bitcoin. The development of digital currencies does not escape this pattern. They are allowed to develop inasmuch as are a source for speculation and profits. Marxists long ago noted that the capitalist economy lives in the contradiction between the progressive socialisation of the productive process and the private accumulation of its results in terms of capital and money. Digital currencies are a big step forward on this path because they would allow a total socialisation of production in a very efficient way. However, it is an illusion to think that this can happen in this current system.

Just before leading the Bolshevik revolution, Lenin wrote a famous pamphlet, The Impending Catastrophe and How to Combat It, where he proposed core measures to allow the revolution to survive and emerge victorious. It is interesting that the first of these proposals concerned the banks. Lenin proposed the “amalgamation of all banks into a single bank, and state control over its operations, or nationalisation of the banks”. He explained that, without controlling the banking sector, controlling the economy was unfeasible. Through the banks, it was possible to keep track of the millions of monetary flows that every day compose the economic life of a country. Controlling the banks allows one to control “the chief mechanism of capitalist circulation [and] would make it possible to organise real and not fictitious control over all economic life”. Lenin also proposed merging all the banks into a single state bank, capable of taking over the clients and functions of the former private banks, and to add many more services in terms of economic regulation.

It is interesting to see how the advantages Lenin envisaged for such a measure are still completely relevant today. For instance, Lenin observed that a state bank for the masses “would be a highly important step towards making the use of the banks universal”: what is now called “financial inclusion” – a goal that international institutions always put hypocritically forward, and even the Libra Association used to introduce its project.

Of course, inclusion is not only an issue of advertising to the people about what a bank is, the point is the cost of banking services. In fact, Lenin goes on to explain that “the availability of credit on easy terms for the small owners… would increase immensely”. It is true that rates on loans have decreased in the last few years due to the intervention of central banks to tackle the crisis, however it is not difficult to find consumer loans with rates of 10 percent or 15 percent, and in specific sectors even more. For instance, the average annual percentage interest rate for payday loans in the US is around 400 percent!

The intervention of a state bank would be decisive in preventing economic strangulation of the poor layers of the population and, with the pandemic, these layers will grow rapidly. Moreover, the universal state bank would put the government in the position to control and regulate economic life, and this is the reason, as Lenin pointed out, “why all the capitalists, all the bourgeois professors… are prepared to fight tooth and nail against nationalisation of the banks”.

This is true today for a state digital currency.

Technology and capitalism

Obsessed with the search for more profits, firms introduce new technologies promising positive change for the population. But this promise cannot be fulfilled as long as their aim is to increase profits. The development of fintech, i.e. the digitalisation of banking and money, is a prototypical case.

We have talked about digital currencies, and how in the present situation, they will be used by big tech to tighten their grip on the world economy and consumers. The gigantic flow of information that is normally called big data, and exploited by artificial intelligence algorithms, can be the base for detailed and effective economic planning on a world scale. For now, they merely propel the profits of big tech sky high.

Digital currencies confirm that the world has outgrown capitalism, but on the basis of this system, they will only enrich the wealthy / Image: Pixabay

Digital currencies confirm that the world has outgrown capitalism, but on the basis of this system, they will only enrich the wealthy / Image: Pixabay

Another example is smart contracts. The idea of a digital contract already existed, but it became easy to create with blockchain technologies. The logic of a smart contract is similar to a cryptocurrency: the software substitutes human actions. This is an efficient step forward, but in the present situation is only beneficial for financial capital.

Let’s give an example. A bank makes a loan agreement with a customer for the purchase of a car based on a blockchain smart contract. The ownership of the car is regulated with a smart contract based on blockchain technology that allows, if the debtor skips the payment of an instalment, the blocking of the operation of the vehicle. After, for example, the delay of three instalments, there is an automatic change in the ownership of the car to the lender. By avoiding the costs and time associated with ordinary administrative procedures (solicitation letters, foreclosure, registration of the new property in the public register, etc.), everything would be done instantly and with no costs.

Who will benefit from these contracts? Smart contracts of this type, preventing the evaluation of the case by a public third party, such as a judge, mean that the weak contracting party (which, between a bank and a consumer, is obviously the consumer) could never assert its own explanation. Cars, houses, and everything else could be taken over by the banks in an instant, with no possibility of discussing the case. Once again, in a capitalist economy, the “smartness” of such a solution, that is efficient indeed, only benefits one side: the capitalists.

A universal accounting system based on a digital currency would make the payment system and economic planning very effective, and artificial intelligence would allow a precise regulation of the productive system. But under the current system, they will only serve the ignoble purpose of making Zuckerberg and the like richer.

Digital currencies confirm that the world has outgrown capitalism. The Economist recently observed that the real risk of these currencies to the financial system, “may be that they eventually precipitate a new kind of run: on the idea that banks need to exist at all” – or capitalism as a whole, we might add.